Manage Your DealersEdge Balance Sheet Turn Your Assets Into Profits - Turn Your Profits into CASH

The Balance Sheet shows how well a business is run, but it is sooo much more.

Every financial statement for every business has an income statement that lists sales and expenses and a balance sheet that lists assets and liabilities.

The Balance Sheet shows how well a business is run, but it is sooo much more. It measures the store’s health, identifies successes and opportunities, and may influence the interest rates you pay and could make the difference between getting another dealership or not.

So, how exactly can a Balance Sheet help dealers appeal to OEMs and banks?

Brooke Samples, President of Profit Blueprints shared her thoughts on how to make your balance sheet healthy, reduce interest rates, improve OEM relations, turn frozen assets into cash and even help qualify for additional stores!

Additionally Brook in conjunction with DealersEdge has created an extensive dealership accounting and operational guide. For more information click HERE

“It sounds extraordinary, but it’s a fact that balance sheets can make fascinating reading.” - Unknown

When it comes to unlocking secrets and suspense, Tom Clancy and J.K. Rowling have nothing on the balance sheet.

In this workshop Brooke explores with us:

How the Balance Sheet is a roadmap to where the profits went… especially if not to cash.

What to do if Working Capital is below recommended value and how to improve your Net Cash position.

How to compare your Balance Sheet to Industry Standards, Historical Trends & Top-Performing Dealer data.

Commonly applied ratios, and what they mean to you, your banks, and the OEMs.

How to create Custom DOCS to monitor your Asset/Liability Accounts; and track and reduce your frozen capital.

What goes into an Emergency Plan?

Why is the Balance Sheet important?

It shows the overall health of your dealership and is important to your manufacturer(s) & lending institutions.

Why do We Need to Manage Cash When We’re Profitable?

Because it is easier to cope with changing conditions that can impact cash flow such as the rising expenses that we are experiencing now, unexpected events and opportunities.

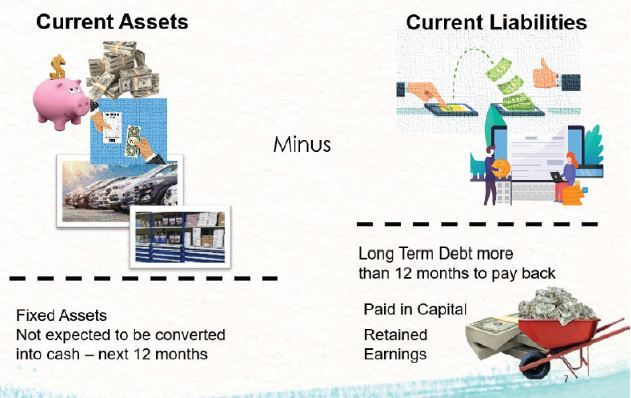

DEALERSHIP BALANCE SHEET

Balance sheets are organized something like this with Current Assets (which can be

turned into cash within 12-months) and Current Liabilities (those expected to be paid within 12-months) “above” the line.

Fixed Assets (not expected to be turned into cash within 12-months), Long Term Debt

(not expected to be paid off within 12-months), Paid in Capital and Retained Earnings “below” the line.

Net Worth is defined as Assets MINUS Liabilities and is a big-picture way to measure your overall financial health.

If You Made a Profit and Your Cash Didn’t Increase… your Balance Sheet is Your Road Map to Where Your Profits Went.

To Be Relevant, Your Financial Statement Must Be:

Accurate

Verify & update counts.

Accounts reconciled.

Complete

Sales & invoices

Accrue payroll.

Timely

Balance sheet is one point in time.

To Be Useful, Compare Lines to Something Relevant such as:

Other balance sheet accounts

Sales

Average monthly expenses

Historical Data – Trends

Your Targets and Goals

Industry Metrics – Automotive & Other

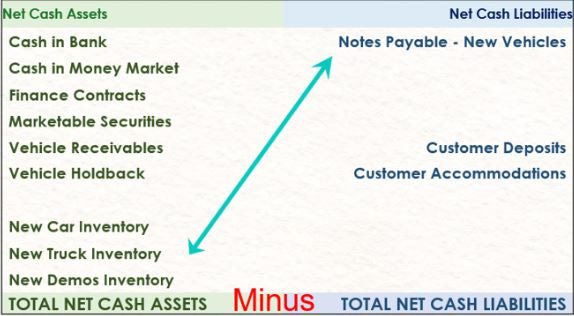

NET CASH

Net Cash is what is leftover when Cash Liabilities are subtracted from Cash Assets

= Net Cash

NET CASH POSITION

CASH ADEQUACY: Determines how much of your average expenses are covered by the Net Cash

NET CASH: $_____ Minus AVE MONTH’S EXPENSES: $_____ = NET CASH POSITION: ______

The Net Cash Position can be either Positive or Negative

NET CASH COVERAGE: Is the percentage of average expenses that are covered by Net Cash.

NET CASH: $_____ Divided by AVE MONTH’S EXPENSES: $_____ = NET CASH COVERAGE: ______

The guide is to be at least 100%

How Would You Improve Your Net Cash Position?

A few examples might be:

Closing Ros or submitting warranty claims?

Collecting receivables?

Sell or floor used vehicles?

Short term loan?

Cash Management Through Asset Management

Why should I bother with asset management?

Once you’ve woven the following actions into your essential practices, you’ll increase your net profits by reducing write-downs or write -offs, have faster selling inventories and save your time for more valuable projects.

Frozen Capital

Even if you have enough cash, more could be tied up in capital that has stopped producing income..

Some sources of frozen capital are:

Excess Receivables

Excess Inventories

Aged Receivables & Inventories

So, why should I care about frozen inventories?

$ If Capital is just sitting, it’s not working for you.

$ Due to cash or space constraints, you can miss opportunities to purchase/stock fast selling items.

$ Increased interest & holding expenses.

$ Potential losses from write-offs, discounting, etc.

Establish Your Targets for Days of Supply for:

Receivables

Vehicle Inventories

Parts Inventory

Work in Process

Sublet

Body Shop P&M

Frozen Capital Guides

S, P, BS Receivables: 50% Current Month’s Chargeable Service, Parts & Body Shop Sales

Warranty Receivables: 25%-50% of Warranty Labor & Parts Sales

New Vehicles: 1.5 Month’s Supply of Retail Cost of Sales (Units or Dollars)

Used Vehicles: 1 Month’s Supply of Retail & Wholesale Sales

Parts Inventory: More Than 35/40 Days & Less than 2 Month’s Supply of Parts Cost of Sales

So, how do I know what is too old and what do I own them for?

Customer Receivables (Aging Schedules)

Warranty Receivables (Aging Schedules)

Used Vehicles (Aging Schedule – Black Book, Etc.)

Parts Inventory Management Reports

Aging and Stocking Status – Benchmark: 70% Active or Normal

CDK: MGR

R&R: 2213

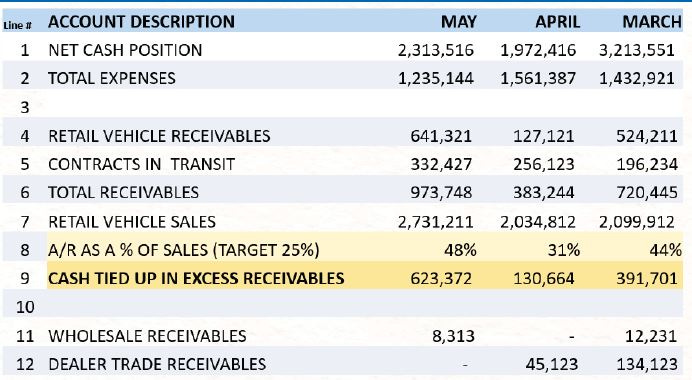

Formulas for Receivables: